Let’s Talk About - The GILT Market

When I was studying for a Real Estate degree back in 1999, I never saw myself writing about the GILT MARKET, and how that might impact my own business and our local economy.

When you are studying for a degree, none of us really know where life’s journey will take us. For me, it led directly into commercial Real Estate for 10 years working in private practice, before setting up GDP in 2011, which works across several fields today, including property, finance, and insolvency matters.

Earlier this week I saw a post on X (Twitter) by one of the leading economic professors I follow online, who was talking about the fact that the interest rate on UK GILTS had broken the 5% mark. I was immediately struck by the potential significance of this, and subsequently over the last couple of days, it has become mainstream news.

What is the Gilt Market?

The gilt market is where the government issues and trades its bonds (“gilts”) to borrow money from investors. These are essentially IOUs backed by the government, typically paying fixed interest over time.

Why it matters to the UK economy

It’s crucial because it funds government spending, influences interest rates across the economy (including mortgages and loans), and serves as a benchmark for financial stability. If confidence in gilts falls, it can raise borrowing costs and create wider economic stress.

The interesting point for me is that the interest rate for many European countries is somewhere between 3% and 3.5%, with the rate on Irish 10-year money sitting at 3.3%, as it is viewed as relatively low risk.

The Burden on Business Owners

For business owners and entrepreneurs, we all know too well what happens when banks and lenders put the cost of money up. The Bank of England sets the base rate in the UK (currently 3.75%), and lenders add their margin on top of that.

When the economy is getting too hot, or inflation is running too high, one of the levers the Bank of England uses is to increase the base rate. This leads to an increase in the overall cost of borrowing money from a bank, creating a direct burden on business owners.

This typically leads to a slowdown in the economy. People become more cautious: they don’t buy that parcel of land, they don’t invest in that new piece of machinery, they don’t hire more people, and they don’t buy that house.

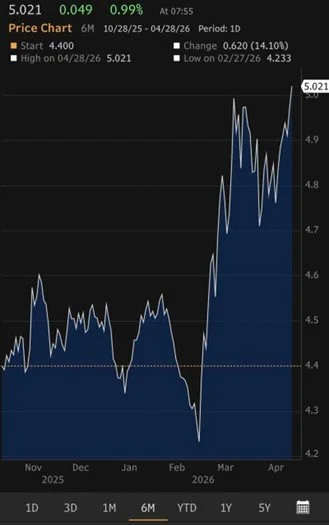

When the interest rate payable on UK GILTS increases—particularly to over 5%—it sends a direct message that investors view the UK economy as much riskier, pricing in that risk by increasing the interest rate. For the UK Government, this is a major issue. If the cost of borrowing increases for them, the only way to counteract that is typically to increase taxes or hope for a wave of economic growth. Looking at the UK growth charts, the synopsis for the next five years is dismal to say the least.

Price Chart for UK GILT Market

Cheapest Money in Town

Despite the more challenging terrain and the macro geopolitical situation, our practice remains highly active. Through our brokerage, Clearpath Finance, we have agreed deals for our client base in Q1 of 2026 to the tune of well over £15,000,000.

On one such deal in the hospitality sector, we recently agreed a facility for over £3,000,000 with a local bank at 2.5% above the base rate. The bank was very comfortable with the asset, the business, and the risk profile, going to a loan-to-value (LTV) of 70%.

The term sheet we agreed on this deal was the cheapest money we have been able to source this year. To be honest, I could have placed the same deal with two other banks who were keen on the business.

The Big Wheel Keeps Turning

My point is that despite the uncertainty and nervousness out there today, business continues. From a liquidity point of view, there continues to be an appetite from the debt market to support solid entrepreneurs who have a good track record and deliverable business plans.

At GDP, we have a wide range of funding solutions available today, comprising both debt and equity options. Whether it is a refinance or new finance you require in the next twelve months—or perhaps you are in distress with your bank—feel free to reach out.

Until next week, look after yourself!

Best,

Conor Devine