The Great Mystery of Money

I have always been interested in money, going back to my primary school days. That fascination stayed with me right throughout my academic career and given I have spent over 25 years involved in finance in one way or another since leaving university, money continues to play an important role in my life.

Questions like what is money? Where does money come from? Who controls the money supply? Does the government have magic money tree’s? These are questions that I would suggest a large part of society don’t know the answer to. I continue to find that very odd!

The Ancient Art of Lending Money — And Why It Still Powers Everything

Money lending isn't a modern invention of course. It's one of the oldest economic activities in human history, and it remains the engine that keeps businesses, households and entire economies thriving and moving forward.

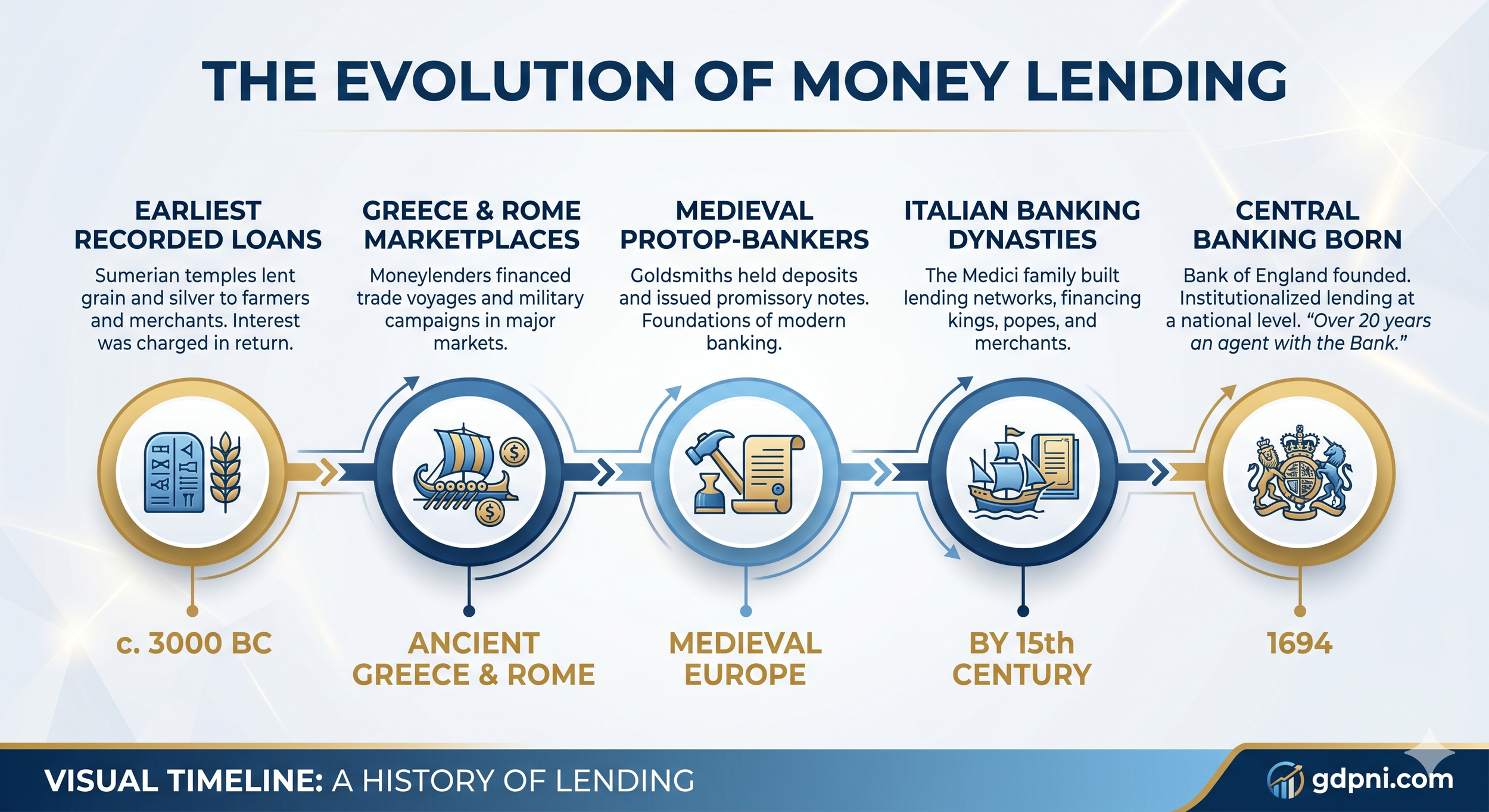

Brief history:

The earliest recorded loans date back to around 3,000 BC — Sumerian temples lent grain and silver to farmers and merchants, charging interest in return.

In Ancient Greece and Rome, moneylenders operated in marketplaces, financing everything from trading voyages to military campaigns.

Medieval Europe saw the rise of goldsmiths as proto-bankers — holding deposits and issuing early promissory notes, laying the groundwork for modern banking.

By the 15th century, Italian banking dynasties like the Medici had built sophisticated lending networks across Europe, financing kings and popes alike.

The Bank of England, founded in 1694, institutionalised lending at a national level — marking the birth of central banking as we know it. On a personal front I have been an agent with the bank of England now for over 20 years, which has most certainly shaped my understanding of money.

Why Lending Is Essential to a Functioning Economy

When James and I started GDP Partnership, there was a huge debt problem in Ireland and across the world. We felt if we could provide our clients with a service that could help them deal with this debt, we could build a successful business.

This chronic bad debt problem led to another huge problem, namely a liquidity / credit issue. As the banking industry had crashed, money lending and entrepreneurs’ ability to borrow money became incredibly difficult, particularly post 2008. This certainly remained a major issue for the next five to six years.

In 2015, and given the liquidity issues across the island, we set up CLEARPATH FINANCE, a brokerage with access to over seventy funders. We thought there would be demand for capital from our clients, if we were able to partner up with the right funders.

For us that exercise proved very successful and today our team at CLEARPATH continues to put funding deals together for our clients, allowing them to continue with their business plans.

The Bigger Picture

Credit markets are the lifeblood of all economies, as business owners are always looking to move forward, buy more stock, create new products, and find new markets. When credit markets seize up (as in 2008), ultimately business starts to slow down.

Access to fair, affordable lending remains one of the clearest dividing lines between economies that grow and those that stagnate. It’s of utmost importance that if the UK economy is to turn the corner anytime soon, and start to experience more sustained growth, access to finance and working capital is key to this happening.

Bank of England

Last week I attended the latest Bank of England presentation, which is always an interesting experience. The good news being it wasn’t as downbeat as I was expecting it to be, given the levels of war, volatility and anxiety we are seeing right across the world today.

Some notable takeaways are below:

There is an ongoing concern about inflation, particularly food and energy prices.

The labour market is loosening up, but still tight in Norther Ireland.

GDP growth is projected to remain weak – 0.2% in 2026.

There are concerns around current consumer spending as that forms huge part of GDP.

The caveat to the presentation was that the Bank of England believe that it’s very difficult to predict what is going to happen in the world over the next three years, so we were encouraged to take the information on board with caution. I did ask the presenter did she mean three days or three years, given how disjointed the world appears to be right now. I think we might have a winner already for “understatement of the year” from the BOE.

Who Is Lending Now?

My own contribution to the meeting last week concerned a very positive development which I have seen continue to play out, over the last twelve months. I am referring to the return of mainstream lenders to the credit markets and their willingness to support local businesses. The caveat here of course being I am only referring to my own experience and that of our businesses who operate in this marketplace.

To give you an example, five years ago, if we had ten loans on the go at GDP, as in organising the funding for ten of our clients, one, or perhaps two of those loans would be funded from the mainstream lenders in Belfast. The remaining 80/90% of the funding would all be coming from the Alternative Lending Market, which has really dominated the credit markets across the UK and Ireland in the last ten years.

Today, Q2 2026, this trend has been turned on its head, as 70/80% of the funding we are arranging for our clients is now being supported by local banks. This is a major change, and I would suggest a very positive development for our local economy. The significance is not lost on me as I haven’t seen this in quite some time, in fact close to twenty odd years.

The other good news currently when talking of banks is that they are very well capitalised today, for the most part have sorted out their legacy debt problems, and balance sheets in rude health.

Despite the challenging environment facing business owners today, the takeaway this week must be that credit markets remain open and quite buoyant, which is a good thing.

Right across our GDP businesses, we are very active raising finance for business owners, particularly those operating in the property markets, healthcare, renewable energy markets, along with hospitality.

-

Until next week, look after yourself!

Best,

Conor